No more Medicaid spend down: What does this mean for me?

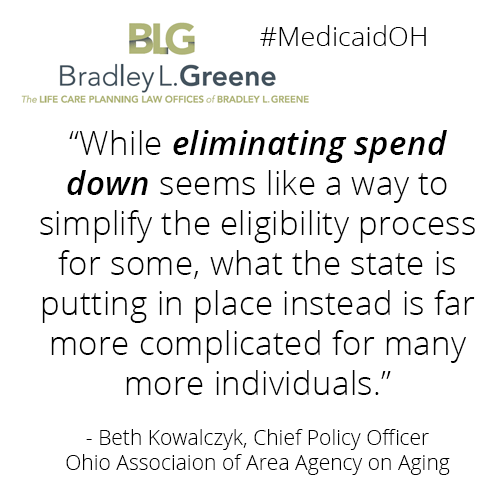

As of August 1st 2016 there are several changes taking place in the state of Ohio’s Medicaid application and eligibility procedures. These changes are intended to simplify the Medicaid administration process, but according to the Ohio Association of Area Agencies on Aging there may be complications and even loss of benefits for some individuals. One of the biggest changes is the elimination of a “spend down” provision that has allowed many Ohioans to deduct health care expenses from their income in order to qualify for benefits.

For example, Jane Smith has a monthly income of $2,699 which is $500 above the 2016 Ohio income limit for Medicaid health coverage. Jane currently provides receipts for $500 a month of medication and medical supplies – which are deducted from her income, placing her below the State of Ohio’s $2,199 income limit. After her “spend down” Jane is eligible for Medicaid coverage and then has 100% coverage for a home health aide through Medicaid’s PASSPORT program (also applies to waiver Ohio Home Care services, nursing home care and Medicaid assisted living coverage).

As of August 1st, with the elimination of the “spend down” criteria Jane will have to set up a Qualified Income Trust (QIT) in order to continue receiving Medicaid PASSPORT services. Her $500 of excess income must be placed in a QIT (sometimes called a “Miller Trust”) to be used only for health care expenses.

According to the Ohio Benefits government website, “Individuals may apply certain deductions to [QIT] funds, and the remaining amount in the trust is paid to the institution or health care providers. On a monthly basis, QIT funds pay for the cost of care, and Medicaid pays for the care not funded by the trust. Upon the recipient’s death, any and all funds remaining in the QIT, up to the total cost of care, are paid to Medicaid.”

The state of Ohio estimates that almost 9,000 nursing home and community residents who are currently on Medicaid will need to establish a QIT in order to continue receiving benefits. This simple online quiz can help you determine if you or a family member fall into this group. Each situation is unique, so if you are unsure about how your current or future benefits will be impacted by these upcoming changes, please call our offices. We are happy to answer general questions and can also help set up a simple QIT trust if necessary.

Please continue to follow us online for more updates on the impending Medicaid changes, and thank you for sharing this information with anyone who might be helped by it.

For example, Jane Smith has a monthly income of $2,699 which is $500 above the 2016 Ohio income limit for Medicaid health coverage. Jane currently provides receipts for $500 a month of medication and medical supplies – which are deducted from her income, placing her below the State of Ohio’s $2,199 income limit. After her “spend down” Jane is eligible for Medicaid coverage and then has 100% coverage for a home health aide through Medicaid’s PASSPORT program (also applies to waiver Ohio Home Care services, nursing home care and Medicaid assisted living coverage).

As of August 1st, with the elimination of the “spend down” criteria Jane will have to set up a Qualified Income Trust (QIT) in order to continue receiving Medicaid PASSPORT services. Her $500 of excess income must be placed in a QIT (sometimes called a “Miller Trust”) to be used only for health care expenses.

According to the Ohio Benefits government website, “Individuals may apply certain deductions to [QIT] funds, and the remaining amount in the trust is paid to the institution or health care providers. On a monthly basis, QIT funds pay for the cost of care, and Medicaid pays for the care not funded by the trust. Upon the recipient’s death, any and all funds remaining in the QIT, up to the total cost of care, are paid to Medicaid.”

The state of Ohio estimates that almost 9,000 nursing home and community residents who are currently on Medicaid will need to establish a QIT in order to continue receiving benefits. This simple online quiz can help you determine if you or a family member fall into this group. Each situation is unique, so if you are unsure about how your current or future benefits will be impacted by these upcoming changes, please call our offices. We are happy to answer general questions and can also help set up a simple QIT trust if necessary.

Please continue to follow us online for more updates on the impending Medicaid changes, and thank you for sharing this information with anyone who might be helped by it.